Payday Super Starts 1 July 2026: How the New Rules Could Impact SME Cash Flow and Borrowing

If you run a small business with employees, or you’re self-employed and employ staff, there’s a significant change coming on 1 July 2026 that’s worth understanding before it takes effect.

It’s called Payday Super, and while it doesn’t increase how much super you pay, it does change when you pay it. And that timing shift? It could quietly squeeze your cash flow in ways that matter when you’re trying to borrow.

So, What’s Actually Changing?

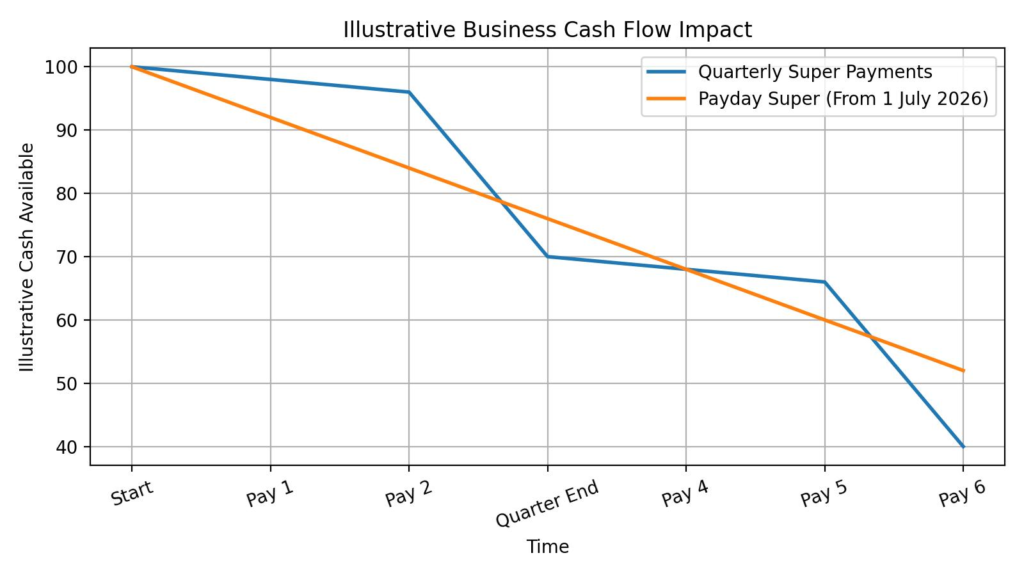

Right now, most employers pay their employees’ superannuation quarterly. Under Payday Super, that changes; super must be paid at the same time as wages, every single pay run.

No more holding that cash for 90 days before it leaves the business.

The reform was passed by Parliament in November 2025 and comes into effect on 1 July 2026. It applies to all employers, regardless of size. The reform is designed to help employees receive their super contributions sooner and to reduce the amount of unpaid super across Australia.

Why Should SME Owners Care?

For a lot of small business owners, that quarterly super window has quietly become part of how they manage working capital. It’s a buffer, money that’s technically owed but still sitting in the account while you wait for invoices to come in, manage payroll, or cover other expenses.

Payday Super removes that buffer. Every pay run now carries a super liability on top of wages. For businesses that are already managing the natural ups and downs of trade, seasonal income, slow-paying clients, and high staffing costs, this is a real shift in how cash flows through the business.

According to a 2025 survey conducted by Prospa and YouGov, nearly four in ten SMEs reported they were not prepared for Payday Super, while one in four were unaware the changes were coming.

What It Means for Borrowing

Here’s where it gets relevant for those thinking about finance or property.

When your day-to-day cash flow changes, it affects how lenders see your business. If your business cash flow appears tighter going forward because super is leaving the account more frequently, it may influence how some lenders assess serviceability and available surplus cash flow when reviewing finance applications. It may also affect how lenders assess business profitability and available cash flow, which matters when you’re applying for a business loan or even a home loan as a self-employed borrower.

On top of that, more frequent super payments may add operational pressure through payroll software, compliance time and accounting support. Those costs affect your bottom line.

How SMEs Can Prepare Now

- Review payroll systems and software.

- Forecast cash flow under more frequent super payments.

- Build additional working capital buffers.

- Speak with your accountant about compliance requirements.

- Review existing lending arrangements before the changes take effect.

How We Can Help

At Safe Haven Finance, we work with a lot of self-employed clients and SME owners, and this kind of change is exactly why we think it’s important to get your finance strategy sorted before you need it, not after.

Ready to take a step ahead? Call us on +61 433 564 936 or book a free consultation; we’d love to help you go into July prepared, not pressured.

You can also follow us on Instagram and LinkedIn for regular finance updates and tips.

Disclaimer: The information in this article is general in nature and is current as at June 2026. It does not take into account your personal circumstances, financial situation or objectives. Lending policies, government regulations and superannuation requirements may change. You should seek professional accounting, taxation or financial advice before making any decisions.