The July 2026 Super Changes Nobody Is Connecting to Your Mortgage: Until Now

If you’ve been thinking about buying a home, refinancing, or investing in property, the super changes kicking in from 1 July 2026 are worth paying attention to. These aren’t just numbers on a government spreadsheet. They directly affect how much you can save, how much you can borrow, and what your financial position looks like when you walk into a lender’s office.

What’s Actually Changing?

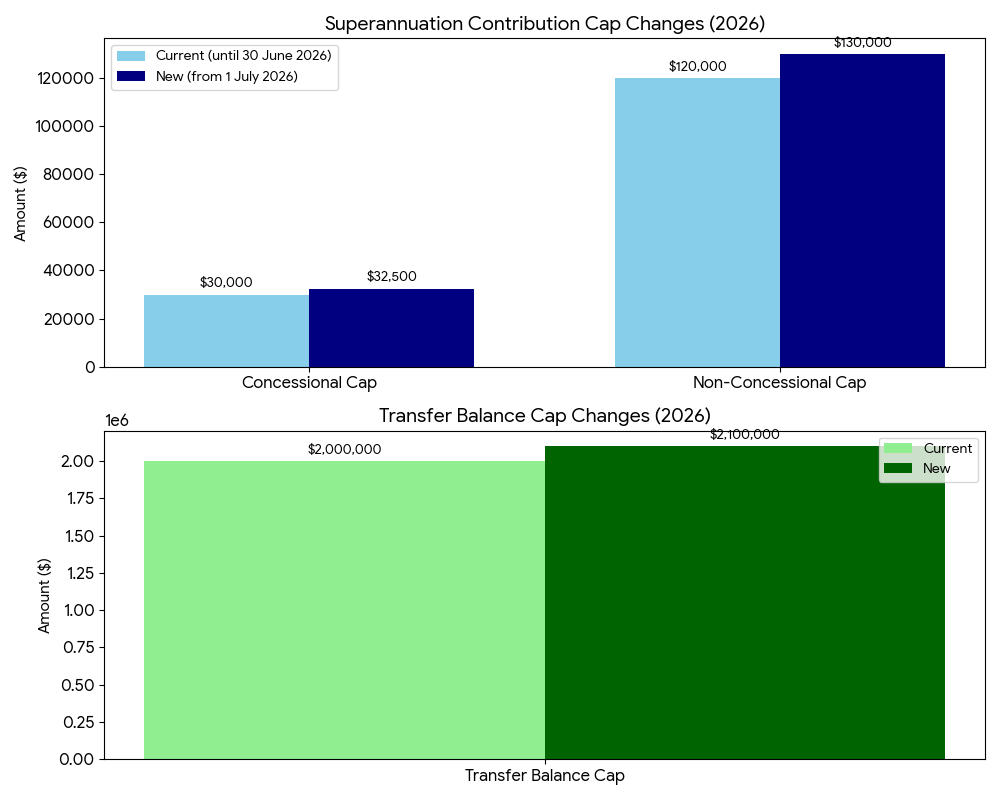

The concessional contributions cap is going up. From1 July 2026, you’ll be able to put up to $32,500 (pre-tax) into your super each year, up from $30,000. This includes your employer’s super guarantee, any salary sacrifice, and personal deductible contributions. That’s a meaningful bump if you’re trying to build wealth tax-effectively before or after a property purchase.

The non-concessional contributions cap is increasing, too. After-tax contributions will now cap at $130,000 per year(up from $120,000). If you’re sitting on savings and want to top up your super before retirement, or use super as part of a long-term property investment strategy, this gives you a bit more room.

The transfer balance cap rises to $2.1 million. This is the limit on how much super you can move into a tax-free pension phase. It’s going from $2 million to $2.1 million, good news for those approaching retirement who are also managing investment properties.

Carry-forward contributions; use them before they expire. If your total super balance is under $500,000, you may be able to use unused concessional contributions from the past five years. Importantly, any unused amounts from 2020–21 will expire after 30 June 2026. This year is your last chance to use them. Don’t let that opportunity slip by.

Payday Super is coming. From 1 July 2026, employers will need to pay your super with every pay run, not just quarterly. For employees, this means contributions hit your super more frequently, which can improve consistency in your financial profile over time.

Source:Australian Taxation Office, Key Superannuation Rates and Thresholds

One Thing to Do Before 30 June 2026

If you have unused concessional contributions from 2020–21, act now. Once 30 June passes, those amounts are gone. Making a personal deductible super contribution before then could reduce your taxable income this financial year, and leave you in a stronger borrowing position heading into 2026–27.

This is the kind of thing that seems small but adds up. Talk to your accountant about whether you’re eligible, and talk to us about how your financial position ties into your property goals.

Ready to Talk About Your Next Move?

At Safe Haven Finance, we take the time to understand your full financial picture, not just your loan. Call us at +61 433 564 936 or book a free consultation. You can also follow us for regular finance tips and updates on Instagram and LinkedIn