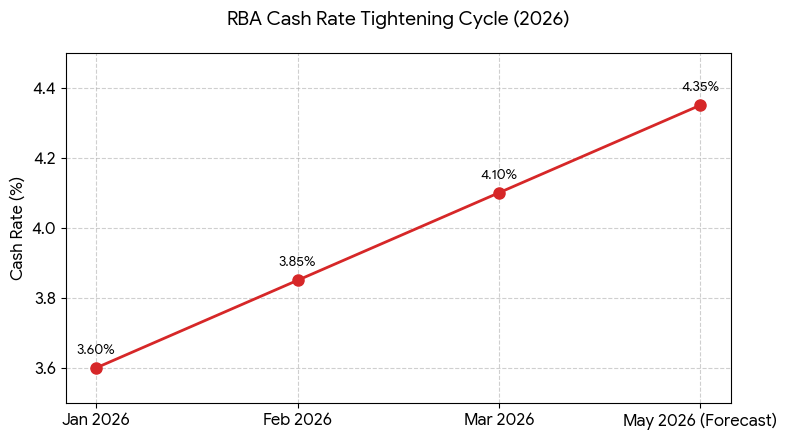

In February 2025, the RBA cut rates for the first time in years. By August 2025, it had cut three times, bringing the cash rate down to 3.60%. Borrowers exhaled. Then February 2026 arrived, and the RBA increased the cash rate by 0.25% to 3.85%. Then, in March 2026, another hike. The cash rate now sits at 4.10%, with all four major banks forecasting at least one more increase in May 2026. If you have a variable home loan in Australia right now, this timeline has directly changed your monthly repayments, possibly more than once in the last six months. Understanding how interest rates affect your home loan is the first step to doing something useful about it.

The Mechanism: How the RBA Cash Rate Reaches Your Repayments

The RBA cash rate is the benchmark at which banks borrow from each other overnight. When it increases, banks’ cost of funding typically rises, and variable-rate mortgage holders often see those changes passed through in the form of higher interest rates.

Following the February and March 2026 rate increases (0.25% each), most major lenders adjusted their variable home loan rates shortly after each announcement. (Source: Reserve Bank of Australia and major bank rate updates)

For example, on a $600,000 variable-rate loan over 25 years, a combined 0.50% increase could add approximately $150–$180 per month in repayments. On a $900,000 loan, this impact may rise to around $230–$270 per month, depending on the loan structure and interest rate.

Fixed-rate borrowers are generally insulated from immediate changes until their fixed term expires. However, borrowers rolling off fixed rates of 2–3% from 2021–22 into current variable rates, which are now commonly above 6%, may experience a significant increase in repayments.

What Rates Actually Look Like Right Now, April 2026

As of April 2026, competitive variable home loan rates in Australia start from around 5.08%–5.13% p.a. for well-qualified borrowers with an LVR below 80%. The average variable rate across the market sits considerably higher, around 6.45%–6.65%. The gap between the lowest available rate and what existing borrowers are actually on is often 0.40%–0.80%, which is the source of the so-called ‘loyalty tax’.

Fixed rates for 1–2 year terms have already priced in the expected May hike and some potential beyond that, meaning locking in a fixed rate now doesn’t necessarily protect you from paying above what you’d pay staying variable. The right choice between fixed, variable, or split depends on your loan size, cash flow, and how much rate uncertainty you can comfortably absorb.

FAQ: How much will my repayments go up if the RBA hikes again in May 2026?

Answer: On a $700,000 variable rate loan, a 0.25% hike adds approximately $90–$100 per month. If May proceeds to 4.35% as all four major banks currently forecast, that would be a combined $270–$290/month increase from the start of 2026 alone on a $700K loan.

Three Things Borrowers Are Doing Right Now And What Actually Makes Sense

Negotiating with their current lender

Banks routinely offer retention discounts to borrowers who call and ask for a better rate before switching. If your loan is above $500,000 and you’ve been with the same lender for 2+ years without a review, calling them and quoting a competitor rate can often result in an immediate 0.15–0.30% reduction without any application or credit impact.

Reviewing whether refinancing makes sense

If your rate is 0.50% or more above the most competitive available rate for your LVR, refinancing is likely to recover its costs within 6–12 months. The key is to calculate the break-even point, total switching costs divided by monthly savings, before committing. Running this calculation is the single most important step before any refinance decision.

Using an offset account to reduce interest daily

In a high-interest-rate environment, an offset account delivers more value, not less. Every dollar parked in an offset reduces the principal you’re charged interest on daily.

What This Rate Environment Means for Buyers and Investors

Rising interest rates in Australia directly compress borrowing capacity. The APRA 3% serviceability buffer means every loan application is stress-tested at your actual rate plus 3%. With variable rates sitting at 6.50%, lenders assess your ability to repay at 9.50%. This is the mechanical reason buyers are finding their pre-approved amounts shrinking and why getting a formal borrowing capacity assessment from a broker before making any property offer is essential, not optional, in 2026.

For investors, the offset strategy becomes even more important; keeping investment loan interest deductible while directing available cash toward non-deductible owner-occupied debt is a structural response to higher rates that many borrowers haven’t been shown. It’s exactly the kind of loan structuring guidance Safe Haven Finance provides across every client consultation.

FAQ: Should I fix my home loan rate before the May 2026 RBA decision?

Answer: Fixed rates have already priced in the expected May hike, so fixing now may not save you money compared to staying variable. It’s a certainty vs flexibility trade-off, not a guaranteed saving. Speak to Payal at Safe Haven Finance before making any changes; the right answer depends on your loan size, cash flow, and timeline.

Safe Haven Finance Your Calm in a Volatile Rate Environment

Payal Varma brings close to 20 years of banking and mortgage broking experience to every client conversation at Safe Haven Finance. When rates move, and in 2026, they’re moving frequently, Payal’s role is to cut through the noise, model what the change actually means for your specific loan, and identify whether action is warranted. Working across 50+ lenders, Safe Haven Finance compares the full market rate, structure, and features to ensure your home loan is genuinely working for you.

Book your free 15-minute consultation call at +61 433 564 936, and your home loan review starts with an honest conversation about where your rate sits today.

Follow Safe Haven Finance on Facebook, Instagram, LinkedIn, and YouTube for regular interest rate updates, home loan guides, and mortgage market insights across Australia.